Make the Most Out of Your Mutual Fund Investments

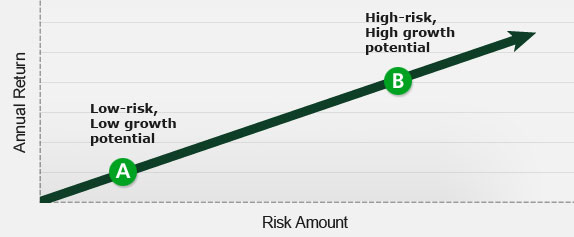

Risk and risk tolerance

One of the basic rules of investing is that the more money you want to make the more risk you may need to be willing to take. This is called the “risk/return trade-off”. It means that a mutual fund with a lot of growth potential can be more sensitive to changes in the market. You might be able to earn more, but there’s a higher chance that you’ll lose more too.

The best way to understand the risk/return trade-off is to speak with a Mutual Funds Representative1. They will guide you through the Customer Investor Profile questionnaire that will help define your investing objectives and your tolerance for risk. Once they understand what you want from your mutual fund investments and your risk tolerance, they will be able to recommend a mutual fund or mutual fund portfolio that is suitable for your needs.

What makes a portfolio low risk or high risk?

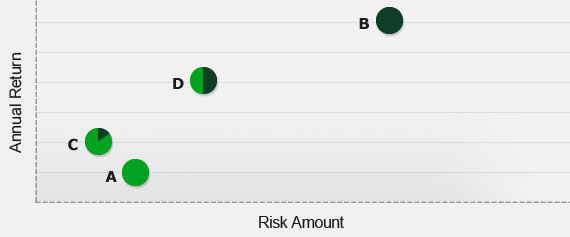

Let’s use the graph above as an example:

- Portfolio A is composed entirely of bonds, which over time experienced both a low annual return ‑ or growth ‑ and low risk.

This is because bonds represent funds borrowed by a company or government in exchange for a predetermined interest rate, and guaranteed return of the principal by the borrower. Bonds generally have less risk than other asset classes, the primary risk being that the company or government that issued the bond could become bankrupt.

- Portfolio B is composed exclusively of equities, which over time experienced high risk and high growth.

A stock is an individual share in a company Stocks ‑ also referred to as “equities” ‑ are traded on exchanges all over the world, and therefore are subject to the dips and rises in the stock market.

- Portfolio C is composed of 80% bonds and 20% equities.

When a mutual fund portfolio includes a mixture of stocks and bonds, you benefit from diversification across these two asset classes.

This portfolio actually experienced lower risk than Portfolio A (100% bonds) and had a higher return.

- Portfolio D split the portfolio, investing 50% in bonds and 50% in equities.

While it experienced more risk than Portfolio A or C, it also got a much higher return as a result.

As you can see there are many options for a mutual fund portfolio. A Mutual Funds Representative with TD Investment Services Inc. will work with you to determine your investment goals and risk tolerance, and then recommend the most appropriate portfolio for you.

Why diversification is a helpful strategy

Diversification can help you minimize your risk, because you aren’t putting all your eggs in one basket. You may also benefit from greater return potential.

So, with a mutual fund, your money is no longer dependent on the performance of a single investment, but instead is an average of the entire collection of investments. That way if one stock or bond ‑ or other asset ‑ in a mutual fund portfolio performs poorly, other well-performing holdings within the mutual fund’s portfolio, may help offset any losses.

The same can be true when investing in more than one type of mutual fund to complete a well-balanced investment portfolio.

One of the best ways to diversify your portfolio is to invest among the three main asset classes:

- Money market

- Bonds

- Equities

Since asset classes tend to move independently of one another, positive performance in one asset class may help offset negative performance in another.

For mutual fund investors, a diversified portfolio could include a combination of money market funds for safety; bond funds for income; and equity mutual funds for potential dividend income and long-term capital growth.

Take advantage of global opportunities

Another important way to diversify your portfolio is by investing in different countries around the world. Often, certain areas of the global economy are performing better than others. In addition, there are industries that may be better represented in other parts of the globe, than they are here at home. By spreading your investments throughout the world, you may reduce your overall portfolio risk, while at the same time increasing your long-term growth potential.

A long time horizon can reduce your risk

Whether you are investing in a bond or equity, they are all subject to fluctuations in market value. Over longer periods of time, however, returns tend to average out and stabilize. Therefore, staying invested longer, helps to reduce your risk and improve your potential for higher returns.

Benefit from dollar-cost averaging

If you can contribute to your mutual fund on a regular basis, not only are you steadily growing your investment, you are saving money while doing so. If you set up a Pre-Authorized Purchase Plan you are investing a fixed amount to your mutual fund at regular intervals.

You may benefit from dollar-cost averaging where you can buy more units when prices are low and fewer units when prices are high. While it doesn’t guarantee a profit, or help protect you against a loss, it can result in a lower average unit cost over time.

For example, let’s say you have $60 a month to invest in a particular fund that fluctuates in price.

January price = $5.00 ‑ You buy 12 units

February price = $3.00 ‑ You buy 20 units

March price = $6.00 ‑ You buy 10 units

In three months, you have invested $180 and purchased 42 units, with an average cost per unit of only $4.29.

Best of all, when you set up a TD Mutual Fund or TD Comfort Portfolio, a Portfolio Manager does all the work for you. So all you have to do is set up a Pre-Authorized Purchase Plan and enjoy the savings.

1 Mutual Funds Representatives with TD Investment Services Inc. distribute mutual funds at TD Canada Trust.

Share this article