@TDAM_Canada

Investor Knowledge + 5 Minutes = Current Insights

The U.S election season is once again upon us and the runoff is set to feature two eerily familiar candidates — the incumbent President Biden and the challenger, former President Trump, who is the presumptive Republican nominee. This election is likely to be one of the most interesting in recent memory as a highly polarized electorate takes to the polls to elect one of two candidates suffering from high unfavourable ratings, both of which have potential stumbling blocks on the road to their respective party nominations.

What's everyone thinking?

According to a recent Pew poll, 26% of American's have an unfavourable opinion of both candidates, with this view especially prominent among voters aged 18-29 (41%) and those without strong party affiliation (averaging 36%) ¹. Part of the reason is increased polarization, but the age of the candidates is also a factor. ²

A March survey by Piper Sandler says that 87% of investors expect a close presidential election and 82% predict a divided government³. Moreover, the contest will feel familiar, as it is a repeat of 2020. This is unusual as Biden vs. Trump 2024 is only the 7th rematch in U.S. history (out of 60 elections) and the first for almost everyone voting this year (the last rematch was 1956, Eisenhower vs Stevenson).

Much ado about nothing?

Before we dig into the investment implications from the election, its important to note that, historically, markets largely have been unaffected by U.S Presidential election outcomes.

The direction of the market, no matter the outcome, is more likely to be driven by fundamental factors like interest rates and corporate earnings. Sure, the possibility for short term market gyrations based on headlines and political rhetoric can be expected, but longer term, asset values and returns are largely driven by fundamentals.

What's in store for markets?

What could a Democratic or Republican party win mean for the macroeconomy and markets? Our thoughts in this blog will emphasize potential policy changes under a second Trump administration, mainly because a Biden re-election would, to a considerable extent, maintain the status quo.

Both candidates are pursuing policies that are inflationary. This includes trade, tariff, and industrial policies as well as an expansionary fiscal impulse. While Trump favours deregulation which is broadly disinflationary, this would be at least partially offset by tighter immigration policies. It is also probable that additional tariffs and higher debt levels could lead to lower medium-term growth prospects and higher interest rates. Among other things, this could raise the likelihood of a fiscal crisis at some indeterminate point in the future.

From a currency standpoint, we also expect a stronger U.S Dollar, especially against the Chinese Yuan. Although Trump has a more extreme form of decoupling in mind, China has been the biggest beneficiary of the hyper-globalization era and will be hit the hardest as we play that movie in reverse. Other countries with a large bilateral surplus could see their economies and currencies face similar challenges.

A Trump victory could provide a short-term boost for equities

The combination of tax cuts and deregulation could result in equity market performance similar to 2017, at least for a brief period. This view is corroborated by a March survey by Piper Sandler which showed that 61% of investors expect the S&P 500 to appreciate if Trump wins³. Such an outcome would be especially probable in the unlikely event of a Red Wave. The biggest sector winners could include tech and financials, as occurred in 2017. We also believe energy would benefit even though it underperformed after Trump won in 2016.

Investors are waiting for the smoke to clear before positioning their portfolios

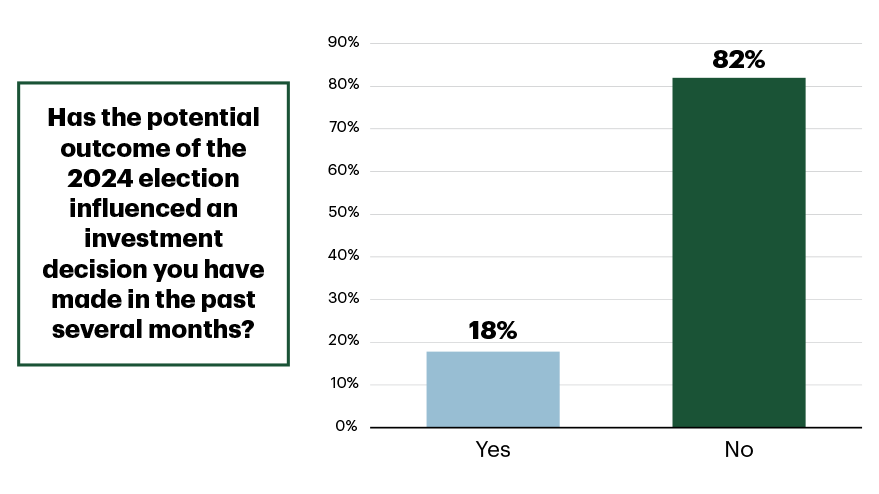

It is also worth noting that, despite of all the attention being paid to the election campaign and the two candidate's economic policies, very few investors have admitted that the election is currently impacting their investment decisions, at least over the past several months (chart below). This appears to reflect the level of uncertainty regarding all three races (the Presidency, the House and the Senate), with investors waiting for more clarity before placing their trades.

The election outcome is not yet influencing investing decisions

"Has the potential outcome of the 2024 election influenced an investment decision you have made in the past several months?"

Source: Piper Sandler client survey (1,086 respondents, survey undertaken mid-March)

Stay tuned for more commentary as we inch closer to U.S election day.

Editor's Note: On July 21st President Biden announced that he will not seek re-election and endorsed Kamala Harris as the Democratic candidate for President. Kamala Harris’s candidacy was confirmed at the Democratic National Convention in August. Policy positions for Harris are likely to remain status quo and very similar to Biden’s.

¹ Pew Research Center survey of 12,693 adults conducted Feb. 13-25.

² Joe Biden, at 81, will be the oldest ever presidential candidate, while Trump will be 78. Since 1789 there have only been four cases where the president was age 70 or higher. Ten were in their forties, 35 in their fifties and 19 in their sixties.

³ Piper Sandler client survey, March 2024.

The information contained herein has been provided by TD Asset Management Inc. and is for information purposes only. The information has been drawn from sources believed to be reliable. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance.

Certain statements in this document may contain forward-looking statements (“FLS”) that are predictive in nature and may include words such as “expects”, “anticipates”, “intends”, “believes”, “estimates” and similar forward-looking expressions or negative versions thereof. FLS are based on current expectations and projections about future general economic, political and relevant market factors, such as interest and foreign exchange rates, equity and capital markets, the general business environment, assuming no changes to tax or other laws or government regulation or catastrophic events. Expectations and projections about future events are inherently subject to risks and uncertainties, which may be unforeseeable. Such expectations and projections may be incorrect in the future. FLS are not guarantees of future performance. Actual events could differ materially from those expressed or implied in any FLS. A number of important factors including those factors set out above can contribute to these digressions. You should avoid placing any reliance on FLS.

TD Asset Management Inc. is a wholly-owned subsidiary of The Toronto-Dominion Bank.

®The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.